Python backtesting infrastructure for systematic strategies

Python library, Rust core. Realistic execution modeling, sub-second performance, reproducible research workflows.

import manifoldbt as bt

from manifoldbt.indicators import close, sma, rsi

fast = sma(close, 20)

slow = sma(close, 50)

signal = bt.when((fast > slow) & (rsi(close, 14) < 70), 1.0, 0.0)

strategy = (

bt.Strategy.create("momentum")

.signal("signal", signal)

.size(signal * 0.25)

.stop_loss(pct=3.0)

.take_profit(pct=8.0)

)

result = bt.run(strategy, config, store)

print(result.summary())Built-in visualizations

ProPublication-ready charts out of the box. Tearsheets, parameter sweeps, risk analytics, all with a single function call.

Execution modeling

The gap between backtest and live performance is driven by execution assumptions. Each component is modeled independently and configurable per venue.

| Dimension | Typical framework | manifoldbt |

|---|---|---|

| Fee model | Flat percentage or fixed cost | Maker/taker split, tiered schedules, per-venue configuration |

| Slippage | Fixed bps or ignored entirely | Volume-impact model calibrated to orderbook depth |

| Funding rates | Not modeled | Perpetual funding rate accrual at 8h intervals, historical rates |

| Borrow costs | Not modeled | Short borrow costs with variable rate schedules |

| Order types | Market orders only | Market, limit, stop-loss, take-profit, trailing stop, partial fills |

| Reproducibility | Depends on random seeds and data snapshots | Deterministic bit-for-bit replay via cryptographic manifests |

Features

Performance

Core written in Rust with Apache Arrow columnar format. Backtest 1 year of 1-second bars in under 200ms.

GPU acceleration

Offload parameter sweeps and Monte Carlo studies to your local GPU, no cluster required. Results are bit-identical to the CPU path (f64, FMA off). Speedup is workload-dependent: up to ~40x on multi-asset sweeps, ~4x on Monte Carlo.

Execution realism

Volume-impact slippage, partial fills, perpetual funding rates, borrow costs, maker/taker fees. Each model independent and configurable.

Research workflow

Walk-forward optimization, parameter stability analysis, 2D heatmaps, Monte Carlo resampling. Deterministic replay via manifests.

Expression DSL

Composable signal declarations, evaluated vectorized over the full series. 45+ built-in indicators including Kalman filter, linear regression, and z-score.

Multi-asset

Native cross-sectional operations: ranking, mean across symbols. Stat arb, pairs trading, and basket strategies out of the box.

Data connectors

Built-in providers fetch and normalize market data into Arrow IPC. Parallel ingestion with progress tracking, import from any source.

Spot & perpetuals

Perpetuals L1

Perpetuals v4 (decentralized)

Spot, BTC, ETH, EUR & USD pairs

Stocks, ETFs, futures, options, forex

CME, NASDAQ, OPRA, tick to daily

All data is stored locally as Arrow IPC (per-symbol, multi-resolution), instant replay, no re-download.

Performance

The engine is written in Rust and operates on Apache Arrow columnar arrays. Data flows through the pipeline with zero-copy semantics and SIMD-friendly memory layout.

Research workflow

A stat arb strategy using Ornstein-Uhlenbeck mean-reversion, built entirely with the expression DSL.

import manifoldbt as bt

from manifoldbt.expr import col, lit, symbol_ref

from manifoldbt.indicators import close, kalman

# Spread construction

pair_close = symbol_ref("ETHUSDT", "close")

ratio = close / (pair_close + lit(1e-12))

# Kalman equilibrium

equilibrium = kalman(ratio, q=1e-4, r=1e-2)

spread = ratio - equilibrium

# OU parameter (mean-reversion speed)

neg_theta = spread.linreg_slope(28)

# Z-score signal

spread_z = spread.zscore(28).ewm_mean(8)

raw = (lit(0.0) - spread_z) * lit(0.05)

signal = bt.when(

(neg_theta < lit(0.0))

& ((spread_z > lit(0.5)) | (spread_z < lit(-0.5))),

raw,

lit(0.0),

)

strategy = (

bt.Strategy.create("ou_stat_arb")

.signal("spread_z", spread_z)

.signal("neg_theta", neg_theta)

.signal("signal", signal)

.size(col("signal"))

)

result = bt.run(strategy, config, store)

print(result.summary())Expression DSL

Signals are declared as composable expressions, evaluated vectorized across the full time series, no Python loops or row-by-row callbacks. Execution is then simulated event by event for realistic fills.

Symbol references

Cross-asset data access via symbol_ref(). Build spreads, ratios, and relative-value signals that reference any symbol in the universe.

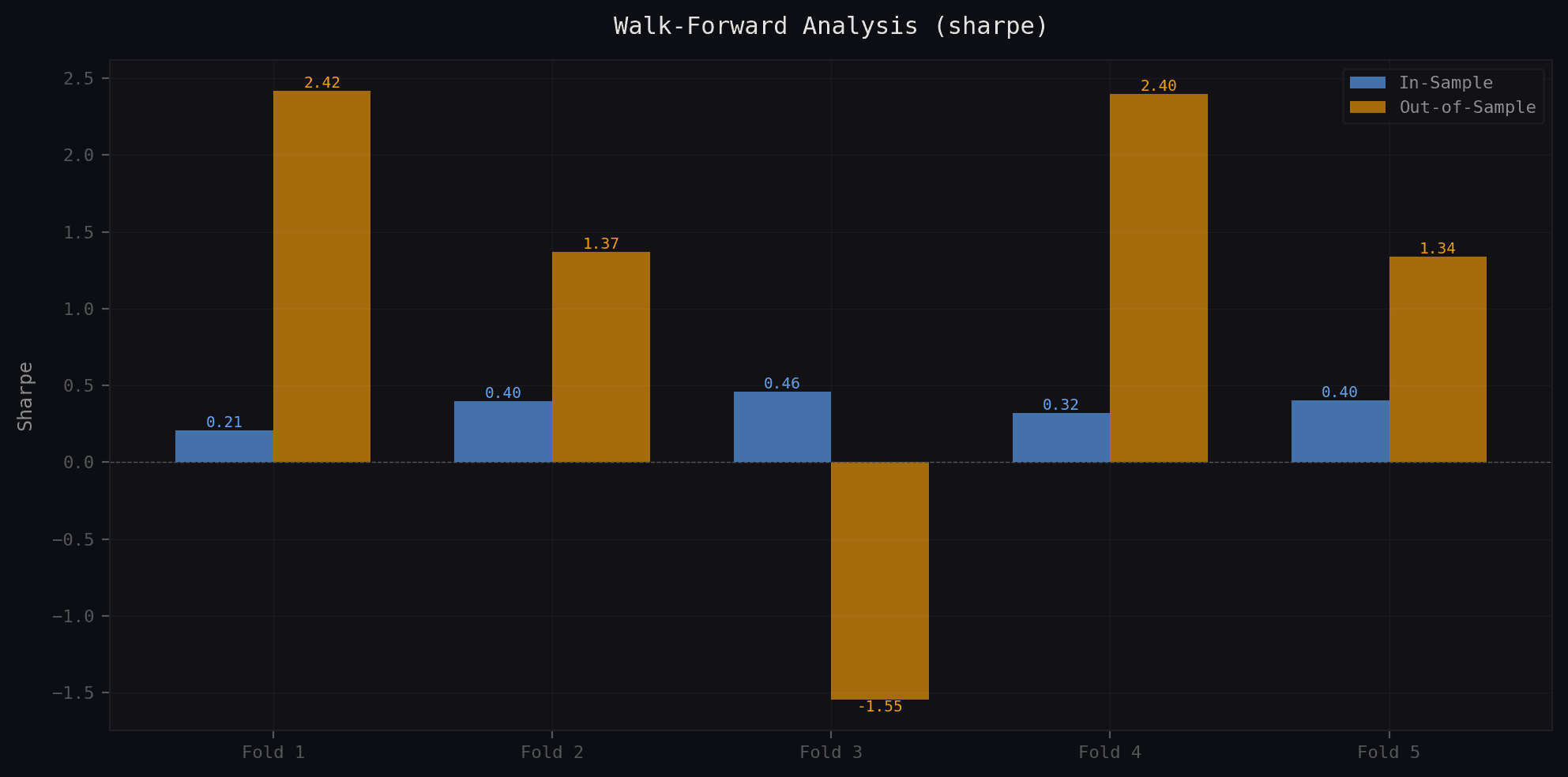

Walk-forward validation

Out-of-sample testing with rolling train/test splits. Parameter stability analysis prevents overfitting to a single period.

Manifest replay

Every backtest produces a cryptographic manifest. Replay any result bit-for-bit, months later, on a different machine.

Research tools

ProBuilt-in tools to validate strategies before deploying capital. Every analysis runs in Rust, no Python bottlenecks.

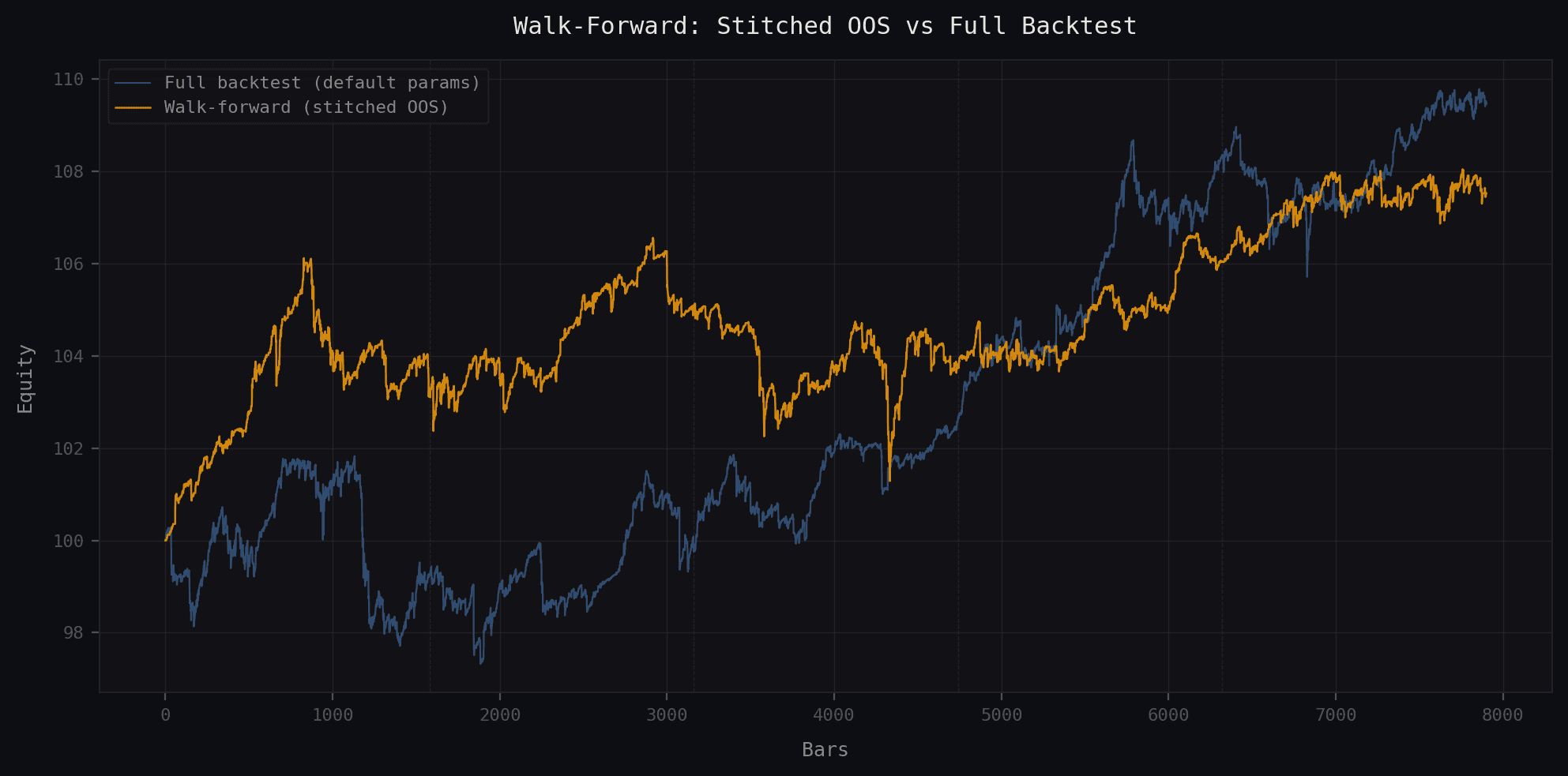

Walk-forward optimization

Split your data into train/test folds. Optimize parameters in-sample, validate out-of-sample. Compare stitched OOS equity against the full backtest to detect overfitting.

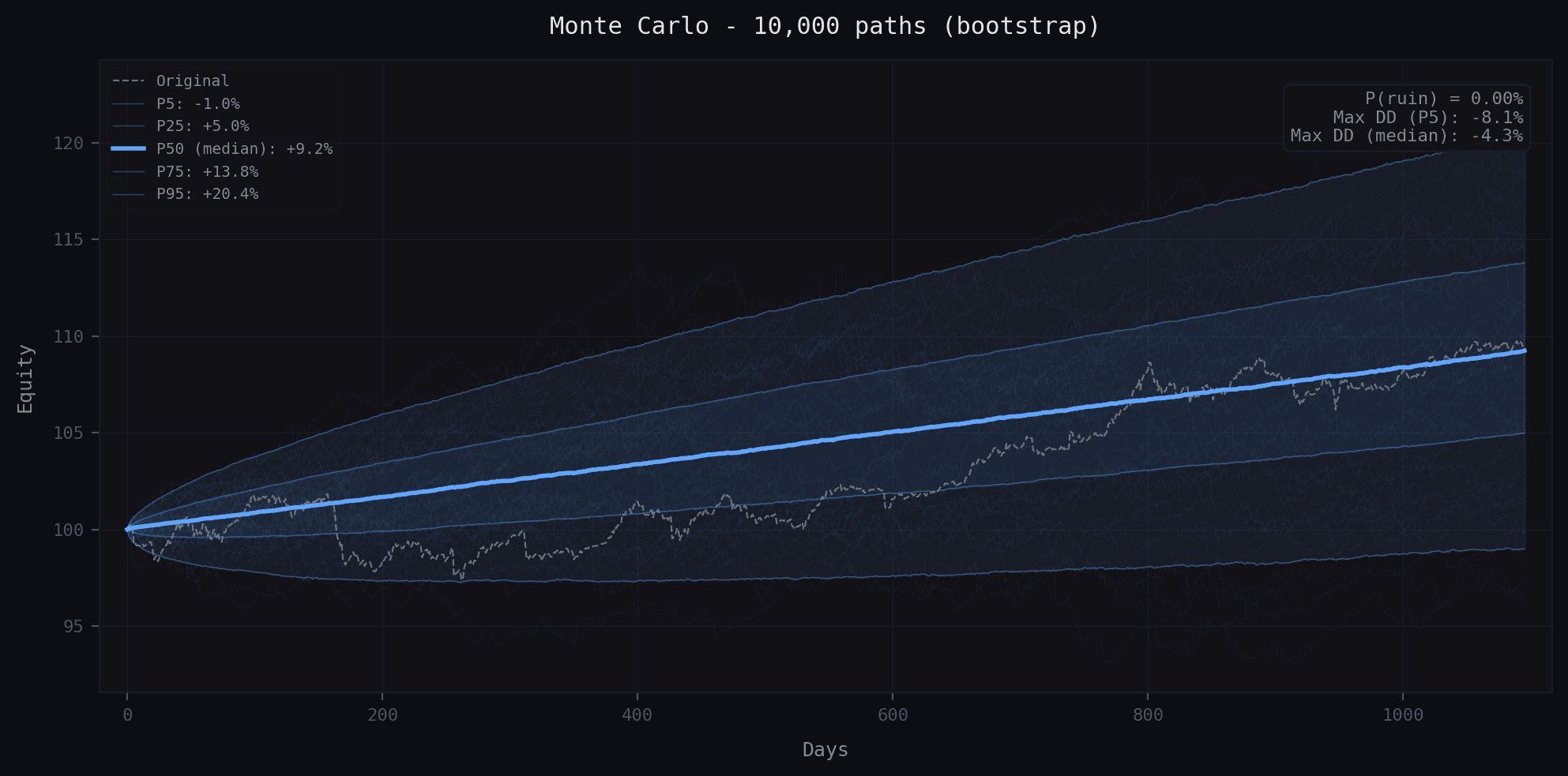

Monte Carlo analysis

Bootstrap returns to estimate tail risk and P(ruin), or permute return order to measure path dependency and drawdown distribution.

Safety checks

ProAutomated diagnostics that catch common backtesting pitfalls. Run them before trusting any result.

Lookahead bias detection

Tests every signal for future data leakage using split-sample comparison. Catches bugs that silently inflate backtests.

$ bt.diagnostics.detect_lookahead(strategy, config, store)Lookahead Bias Detection Report================================Method: split-sample comparison (5 split points)Tolerance: 1.0%Signal 'fast' no future data okSignal 'slow' no future data okSignal 'rsi' no future data okSignal 'entry' no future data okPosition sizing no future data okResult: CLEAN - no lookahead bias detected

Exposure stability

Verifies that strategy exposure is consistent when you extend or truncate the backtest period. Detects regime-dependent behavior.

$ bt.diagnostics.check_exposure_stability(strategy, config, store)Exposure Stability Report=========================Extension test (2/3 -> full): drift = 0.3% okTruncation test (full -> 1/3): drift = 0.8% okRegime sensitivity: stable across 3 windowsResult: STABLE - exposure consistent across time ranges

Pricing

- Rust-powered engine

- All 45+ indicators

- Multi-asset

- Parameter sweeps

- CSV import

- Engine resolution: 1m

- Timeseries output: Daily

- Monte Carlo resampling: 1,000 sims

- Crypto connectors (Binance, Bybit)

- MCP server (AI agent integration)

- Rust-powered engine

- All 45+ indicators

- Multi-asset

- Parameter sweeps

- CSV import

- Engine resolution: 1m

- Timeseries output: Up to 1m

- Monte Carlo resampling: Unlimited

- Crypto connectors (Binance, Bybit)

- MCP server (AI agent integration)

- Databento & Massive connectors

- Built-in WFO

- Safety checks (lookahead, exposure)

- Tearsheets & export

- GPU acceleration

- Rust-powered engine

- All 45+ indicators

- Multi-asset

- Parameter sweeps

- CSV import

- Engine resolution: 1m

- Timeseries output: Up to 1m

- Monte Carlo resampling: Unlimited

- Crypto connectors (Binance, Bybit)

- MCP server (AI agent integration)

- Databento & Massive connectors

- Built-in WFO

- Safety checks (lookahead, exposure)

- Tearsheets & export

- GPU acceleration

- Managed compute

- Hosted data (Databento, Massive)

- Team licenses (5+ seats)

- Priority support

- Custom integrations (data sources, indicators)

FAQ

Learn backtesting in Python

Step-by-step guides, runnable strategy walkthroughs, and honest comparisons, all built on realistic, reproducible backtests.

Guides

- How to Backtest a Trading Strategy

A step-by-step Python walkthrough: from raw bars to a realistic backtest and a tearsheet.

- What Is Backtesting?

What backtesting is, why it works, where it lies to you, and how to do it honestly in Python.

- Algorithmic Trading in Python

The libraries, the workflow, and a runnable parameter sweep to research systematic strategies.

- Walk-Forward Optimization in Python

Optimize in-sample, validate out-of-sample, fold by fold, the honest way to tune parameters.

Compared to other libraries

- Manifold-BT vs Freqtrade

An honest comparison: fast, realistic backtesting versus live crypto trading, and when to use each.

- Manifold-BT vs vectorbt

Rust engine with vectorized signals and event-driven execution, versus vectorized NumPy: speed, realism, path-dependent logic.

- Manifold-BT vs Backtrader

A fast, realistic research engine versus a mature pure-Python framework, and when each fits.

Or browse 15 Python trading strategies, each with runnable code and a backtest, see all strategies →